Find your perfect college degree

Most college students today feel genuinely unprepared when it comes to managing their finances. According to a recent survey conducted by EVERFI, most college students have already accumulated debt in recent years.

The report presented, called “Money Matters on Campus,” was sponsored by AIG Retirement Services. The study sought to assess college students’ financial understanding and capability as they prepare to take part in the workforce. It surveyed more than 30,000 college students from 440 colleges and universities scattered across 45 states.

According to the report, 6 in 10 students have already taken or planned to take out loans to help cover the exorbitant tuition bills. Sadly, only 65% plan to pay off their debt in full and on time religiously.

EVERFI’s president and co-founder, Ray Martinez, strongly believes that so many American families are not fully aware of the real cost of going to college. This eventually results in students taking out loans simply because they come to college unprepared financially.

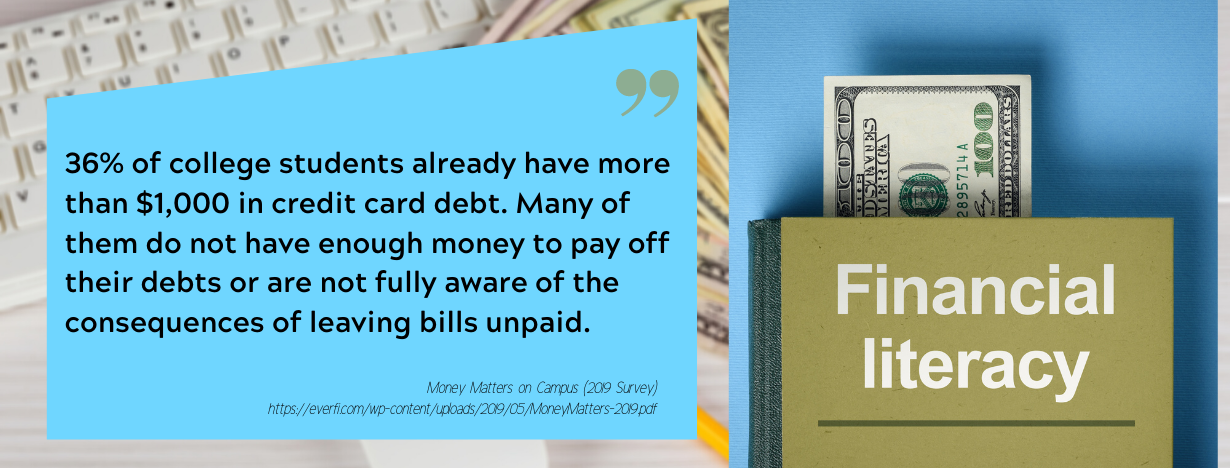

Apart from students struggling with their student loans, most of them also face other issues with paying back their credit card bills. The survey further showed that 36% of those who participated already had credit card debts, not less than $1,000; most were not aware of the critical consequences of having their bills left unpaid.

These alarming figures all boil down to one thing: the lack of financial education. Dr. Daniel Zapp, the senior director of research at EVERFI, reiterates that it’s important for financial education to be consistent for it to stick—just like any form of education.

He said nobody would learn math seamlessly if we only took a single mathematics course. Because of continual courses built upon each other, plus the reinforcement of the knowledge we previously learned, we have successfully developed a true understanding of the subject.

Based on the survey, only 17 of the 50 US states need a personal finance course as a prerequisite for high school graduation. Of these, only seven will require actual testing of one’s financial skills before graduation. Plus, only 35% of college students took personal finance courses during high school.

So, just how important is financial literacy for college students?

The Bureau of Consumer Financial Protection released a report sometime in September 2018 called Pathways to Financial Being: The Role of Financial Capability. It was noted that one’s financial behavior corresponds to one’s financial skill and self-efficacy.

Defined as your perceived financial security, your financial well-being strongly depends on your financial life’s objective facts, alongside your capacity to efficiently manage your finances.

While most retired and employed people fully understand the importance of financial literacy, you, as a student, should be prudent enough to learn more about the subject. Here are some reasons why financial literacy is an imperative subject matter that every college student should learn.

Being Financially Literate Affects How You Look at Money in the Future

The Federal Deposit Insurance Corporation studied the effects of financial education on one’s self-confidence about properly managing money and actual behavior.

In a program they conducted, 69% of their participants admitted that following the program, they improved their savings after fully understanding how to save effectively. 78% said they now own a checking account, a 12% jump in student participant outcomes before taking the program.

This is a clear example that a student’s financial literacy will never come naturally. It needs proper training and ample guidance to affect your financial behavior fully. Say, for instance, an academic essay assignment. This is a very tempting project that often encourages students to spend money.

Instead of putting effort into making the task, most students will rather pay for someone to make it for them. As meager as the project may be, this will dent and affect your monthly budget. Of course, the advantage here is that you will surely pass the assignment that you know you will fail otherwise.

A financially literate student will only Edubirdie when he feels it is necessary. But if you have time for the task, why not work on it yourself and avoid paying for somebody to write for you?

Those who lack financial literacy will only procrastinate working on the paper, believing that these tasks are easily available online. You see, your being smart about money will make a huge difference.

Your Negative Spending Habits are Balanced Out if You are Financially Literate

Did you know that college students are three times more addicted to gambling than adults? Although most colleges and universities have strong policies against on-campus drinking, gambling awareness is more lenient.

Only 22% of all colleges across the US have anti-gambling policies. Most schools fail to block online casinos, resulting in students freely spending their money on gambling sites.

But if you are financially literate, you know you can stay away from negative financial behaviors like too much alcohol or excessive online gambling. You are fully aware of how you plan your monthly budget and understand the risk you get if you fail to follow your budget plan.

From missed due dates of utility services to low budgets on food and coursework materials, all these are put at risk when negative spending habits are practiced.

As for the extra cash, you know you can spend it any way you want. But if you are money-smart, you understand that putting your extra money into a savings account is the best approach.

You Will Learn More About Taxes

When talking about financial literacy among college students, the first thing that pops into mind is how you can effectively budget your monthly finances. This is a relatively acute problem that every student should deal with. Did you know that it’s just as important to learn about taxes?

Some students have part-time jobs that help them earn money to pay for their college tuition. Those with traditional jobs can handle the taxing part easily.

But what do you work on those with freelance jobs like makeup artists, graphic designers, photographers, and all those non-traditional jobs? Did you know that you need to file your taxes as well? Most freelancers aren’t aware of how to do it. Taxing is not taught in high school.

This is where college professors come into the picture. Professors must encourage college students to learn the basics of taxes. The regulations and laws have to be taught and discussed. Sure, earning money gives you a lot of perks, but this also comes with responsibilities. If you know how to manage your finances very well, then taxes won’t be an issue.

College Students Must Understand How to Deal with their Finances

University life is probably your very first chance to be independent. Back during your high school years, your parents gave you pocket money and allowances and managed your finances themselves.

Should you have extra money out of these allowances, you would usually use it to buy new clothes or hang out at your favorite dining spot. But with college, everything changes. Everything comes with responsibilities.

The Top 9 College Financial Literacy Programs

Because of the continuous rise of college costs, financial literacy programs have become necessary for college students to handle their finances responsibly, like their student loan debts, among others. Recent data reveals that the outstanding total of student debt as of 2023 is $1.7 trillion. Today, there are more than 45 million student loan borrowers.

These student loans, coupled with thousands of students being financially illiterate, have prompted some schools to offer programs to educate students in dealing with their finances.

Here are ten of the best colleges and universities that offer financial literacy programs.

Texas Tech University

This school has one of the best financial literacy programs. Called the Red to Black program, they offer presentations, workshops, and personalized coaching covering topics like maximizing student loans and creating spending plans. The program’s objective is to teach students to succeed not only academically but financially as well.

George Washington University

GWU is notable for its modern financial literacy program. This university plans to impose a mandatory financial literacy course across the US and has invested a significant amount of time and research into the topic. They also are very active in academics, and they hold discussions with policymakers. All in all, GW is active in promoting financial literacy for college students.

Syracuse University

This school has so many events prepared for its students to join with a financial incentive attached. It runs a money awareness program featuring grant funding. Qualifiers are also obliged to take mandatory financial literacy sessions.

They also have money coaches available on a one-on-one basis should you need a more personalized session. Guides and resources are available on the program’s online site to allow students to start managing their finances easily.

University of Montana

The University of Montana offers its undergraduate students an online financial literacy program called Transit. Other programs are also provided and often include FASFA guidance, student loans, and budgeting workshops. Students also have access to free and private sessions.

Sam Houston State University

SHSU’s financial literacy program has a huge staff of students and professionals to help those in need. Scholarships are also provided every year and are awarded mostly to those who remain active in the program by joining events and workshops. The program also has a financial education application called CashCourse.

Duke University

Duke University created a well-designed program under the Office of Personal Finance. Here, one-on-one counseling and seminars are provided.

This program’s primary goal is to offer opportunities and workshops in financial education so that college students will be more educated and well-versed about their financial goals and finances. Duke University also has a very well-built dedicated website that you can seldom find in many other programs.

University of North Texas

The University of North Texas has a financial literacy program that provides events, coaching, and other emergency aid programs. The University of North Texas financial literacy program (Student Money Management Center) provides outreach events, coaching services, and an emergency assistance program to students.

The university is also proud of Mean Green Money, a student-driven financial literacy podcast that talks about different personal financial topics and personal experiences shared by students, alumni, and content experts.

Southern Connecticut State University

Southern Connecticut State University offers more than 100 workshops annually, discussing purely financial literacy and education. The most common workshops include Budget Talks, Paying for College, and Life After College.

Also, the school features more than 4,495 individually created personalized financial advising programs for students. You can see several other resources on their centralized websites, such as recommended readings, student discounts, and videos.

University of West Florida

The University of West Florida has the Louis Maygarden Center for Financial Literacy, which was created to help the school’s community and its students learn more financial knowledge and properly deal with their finances. Everyone in the community can seek free credit counseling, workshops, CashCourse, and certificates for financial literacy competency.

10 Lessons in Financial Literacy Every College Student Should Learn

Try asking a mid-life about what it is that they wished they had learned in college. Chances are, they will tell you they wished they’d fully understood what financial literacy means. After all, being financially knowledgeable means these mid-lifers would have been more successful in life.

As you prepare your way for college, it’s normal to keep your attention on things you believe will truly matter: Greek and dorm life, academic plans, or extra-curricular activities. However, academic advisors say you should also focus on your finances.

Remember that your college years are the best time to learn smart money-spending habits, start building your credit, and learn how to manage your debt and budget. Thus, whether you are an incoming college freshman or already deep into college, below are some lessons financial advisors will recommend you should learn.

Deeply understand your college financing.

Rita Cheng, a financial advisor from Blue Ocean Global Wealth based in Maryland, said it’s surprising how students fail to understand how they are paying for their college tuition and how much this will impact them in the future.

Most college students do not know the difference between the loans they are borrowing versus the scholarships and grants they are receiving and which between these are tied to a minimum GPA and other requirements.

As you set your foot in college, it’s best to understand these financial vehicles deeply. Know the difference between a college loan and a college grant. That way, you’ll be able to set realistic priorities while in college. You will also learn more about the value of the education you are having.

Know where your money is going.

It’s a given fact that most college students are always cash-strapped. Unfortunately, so many students also spend their cash on unnecessary experiences and products—weekend travels, pizza, lattes, and concerts. If you wish to make the most out of your college life, it’s best to know where all your money is going.

Be wary of your spending- whether it’s for textbooks and school projects or take-out budgets. Keep a list or practice using an app or an online tool to track your expenses because this will help you make better and more informed decisions about your money spending as time goes by.

Understanding your budget is the key to succeeding in your next lesson: saving. How so? Because the money you set aside for savings is likely to depend on how you trim your “fun money” and other unnecessary expenses.

Save, save, and save.

Setting aside about $100 a month via a savings account or through market investments (funds or stocks) can give you so many benefits in the end. Initially, you may think a meager amount won’t vary that much. But if you look at its long-term benefits (a decade or more), your savings habit will help you create a safety net.

Say, for instance, you start to save $100 per month for four years, with a typical annual interest rate of 1.3% (the usual rate for a savings account). In four years, you will have $5,028. Perfect gift for yourself right after graduation, right?

Study how student loan debt works.

Avoid taking out student loans that you know you don’t need. This is a very common mistake among college students and could lead you to overspend on your education budget.

Some students may not even know which college debt they are using and which one their family may be taking care of them. You may not know that you will be required to start repaying your loans just six months after your graduation unless you can satisfy specific loan conditions (further education, unemployment, forbearance agreement).

And if you fail to double-check your student loan using a debt repayment calculator, you may end up paying like what one pays in a car (or even mortgage) loan!

Thankfully, most student loan lenders give young adults a reasonable payment scheme that won’t exceed a specific fraction of their income.

Not all debts are bad. Poorly managing your debt is.

You might know the “freshman 15.” But what about the “senior $1500?” That is the debt you get upon graduation if you carelessly sign on to different high-interest credit cards the moment you enjoy your freshman years in college.

Remember, having this much debt with double-digit interest rates will leave you at a loss come payment time, especially if you’re still on entry-level work.

But don’t fret. Not all debts are created the same. You have the ‘good debts’ like auto loans or student loans that you know you can repay at a set price at a given time. Credit cards are not bad debts as well, so long as you know you can religiously repay the credit and its charges. If you plan to carry a credit card, understand their terms first and look around for the best ones suitable for your needs.

Build your Credit Standing.

It is terrible to go beyond your credit card limit, but there are adverse consequences if you also fail to use it. Why? Because the more you use your credit card, the more you build your credit card score. In the future, getting an auto loan, a lease, a small business loan, or a mortgage loan will heavily rely on your credit score. Plus, employers will check your credit score to gauge your jobworthiness.

Therefore, college is the perfect time to start using a credit card wisely and responsibly. Having a credit card and other types of loans that you can religiously pay will help you create a good track record.

Although other lending platforms evaluate non-credit metrics (grades, academic standing, or alma mater) to check whether you are loan-credible, old-school credit standing remains very helpful across almost all types of loans.

Understand Opportunity Cost.

Enrolling in college is a critical step for most young adults. However, with the never-ending increase in tuition costs, coupled with left and right student loan debt, very competitive job markets, and pricey rents in key areas where fresh graduates are expected to look for jobs, no doubt college is indeed a financial minefield.

For many students, college is their first lesson in “opportunity cost”—the boons and banes of different choices. Borrow too much, and you will end up getting a high loan debt later. Work your heart out to cover your tuition fee, and you will find yourself too drained to even think about opening your books and studying your lectures.

Learn how student loan refinancing works.

Only a few percent of college students graduate without a student loan debt. If you are left with student loans upon graduation, understand that your debt can be refinanced via different programs. It’s important to know these options well before you graduate.

Some programs may need you to have strong credit records, or maybe you should have savings to make an initial payment to help minimize your total debt balance. But do not assume that you are automatically eligible for the different advertised refinancing programs. Ask around to find the best deals.

Think about your work experience.

Even if you’re juggling between work and school, don’t toss your report card overboard or avoid socializing with friends simply because you are so focused on earning money to compensate for your tuition.

It’s important to build social networks while you’re on campus. Find a job that closely ties to the future career you have in mind or something that conveys office skills related to many future fields.

While grades are indeed important, social capital and real-world experience are just as critical. Thus, if you are working in college, try to be intentional about earning money. For instance, if you’re a budding psychologist, look for jobs at your local crisis hotline. Or, if you dream of becoming a journalist, get a paid job at a local newspaper.

You can use loans to support your well-thought-out university experience.

Is it okay to work for hours at a job that you know can help you subsidize your college tuition so that you can reduce your student loans? Or do you prefer to focus heavily on your academic performance, so you opt to tap higher student loan amounts so you can still join extra-curricular activities in school, study overseas, or even get low-paid but highly informative internships?

This is a very hard choice. However, college advisers suggest that you can focus more on your social network and your grades while in college. And if your finances will cut it, go for pre-professional internships.

The social and professional connections you make, even at this early college stage, are extremely valuable over time. This will give you an edge as you start your career after college.

Straightforward Money-Saving Tips for College Students

To have a solid financial foundation in the future, you should learn how to manage your money smartly. Since college is when you start to gain financial independence, here are some tips to help you save and make smart and intelligent choices about your spending.

- If possible, avoid student loans. Many college students make the greatest mistake of taking out student loans more than they need. While these loans are not always avoidable, do your hardest to take out only minimal loans if you do need one.

- Avoid spending more than what you’re earning. This is the most powerful money-saving tip that, to this day, is still a challenge to many.

- Make a budget. This simple but very powerful tool allows you to keep close track of your money spending. You can find a lot of online budgeting apps and tools, as well as spreadsheet templates, to get you started.

- Create a plan to deal with your debt. If you take out more student loans than you need and other personal loans and credit cards, make sure you know how you will handle your debt.

- Limit your credit cards. It can be tempting to take out numerous credit cards, knowing that these can also be good financial tools to build a better credit score. However, if not widely used, credit cards can also be very dangerous. Avoid having so many cards if possible, and ensure that all your balances are paid on time.

- Start to invest now. The earlier you decide on investing, the more time that your investment will have to gain interest. Investing is easy. Open an online account with some of your savings and make deposits regularly every month.

- Have an emergency fund. For optimal financial health, you need to have an emergency fund. You will never know when you will need money for an unexpected medical emergency or when your car breaks down. If you are in the middle of paying your debt, you can start a smaller emergency fund. The goal here is to have something that you can use during emergencies.

- Know the type of insurance you need. You can find so many types of insurance products today. But being a college student, know what type of insurance you need. You don’t need life insurance if you’re single and don’t have any children yet. But do you need auto insurance, health insurance, or maybe a renter’s insurance? These things have to be secured in place so that you know you will be protected.

You spend four years of your young adult life trying to invest in yourself. Financial advisors call this “human capital.” College life is where you start to build your social network and learn initial job skills, and your professors might even provide you with references that will surely help you jumpstart a budding career right after graduation.

There will always be so many ways for you to take advantage of what college life has to offer. Among all the crucial factors to becoming successful in your chosen field, managing money carefully and practicing financial literacy are vital lessons you must learn.

Additional Information: